February Posts $48bn as Volatility Subsided (Erb/Manzi)

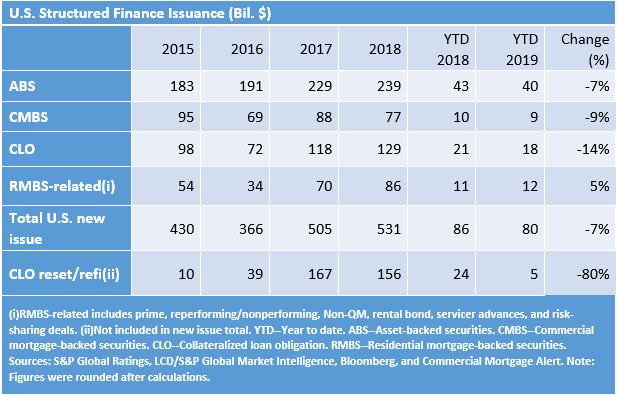

U.S. Structured Finance (SF) Issuance picked up in February as the market volatility that characterized much of the Dec./Jan. period subsided. Led by the ABS and CMBS sectors, February issuance totaled $48bn, up from $32bn in Jan. Total new issue volume for the first two months of the year was $80bn, down about 7% from the same period in 2018.

ABS issuance was $23bn in February. Accounting for over half of that figure was auto ABS, which came in at nearly $14bn. February auto ABS issuance was over double last February’s total. On a YTD basis however, 2019 auto ABS issuance is only slightly ahead of last year’s figure because of the aforementioned slow January. YTD ABS issuance reached a little over $40bn this month, down from $43bn last year. To view our latest ABS commentaries, including a 10-year retrospective on auto ABS, a whole business ABS frequently asked questions paper, and a look at the true lender conundrum in marketplace lending, click here. For the latest auto loan ABS tracker, click here.

CLO new issuance was $13bn in February. On a YTD basis, overall CLO new issuance reached $18bn this month, down 14% from 2018's result. CLO resets and refi’s have been much lower this year and are currently at less than $5bn in issuance, down about 80% on a YTD basis. Click here to view our recent CLO publications.

Led by strong conduit issuance, February CMBS new issue volume totaled $6bn, doubling the January figure. Conduit issuance was $5bn in February versus none in Jan. YTD CMBS issuance is just over $9bn, down about $1bn from 2018’s figure. (Note: We do not include CRE CLOs in our CMBS totals.) Click here to view our recent CMBS publications.

Following nearly $6bn issuance in February, Private Label RMBS issuance is now $12bn YTD, up 5% y/y, and the only major sector that can claim a gain so far this year. Non-QM issuance YTD is up nearly $3bn from last year’s figure, which was just over $1bn. Click here to read our recent RMBS related publications including Will the Froth in the U.S. Housing Market Bubble Over? We Think Not.

Turning to the Numbers...

The 10yr Treasury was 2.75% for the week ending March 1, up from 2.65% last week. NYMEX crude oil was down $1.51 w/w to $55.75. U.S. regular gas prices averaged $2.42 this week, up 4 cents w/w and down 12 cents y/y. The S&P 500 was up 0.39% w/w to 2803.69. The 30-year fixed-rate mortgage was unchanged w/w at 4.35% (down 8bps y/y). The Euro was trading at $1.1367, up $0.0032 w/w.

Recent Short Articles (available here)

U.S. Structured Finance Issuance: January Was Slow to Start, But Picked Up Steam Heading Into February

Four Ratings Raised, 232 Ratings Affirmed On 17 U.S. And Canadian Credit Card ABS Trusts

Buyer Beware: The Curious Case of Income Supplemented BTL

New Commingling Reserve Mechanism in German Auto ABS Requires Further Considerations in Our Cash Flow Analysis

Fewer Structural Protections in Today’s Speculative-Grade Subprime Auto Loan ABS

Single-B Subprime Auto Loan ABS Gain Popularity as Industry is Poised for Consolidation

Recent In-Depth Articles (available here)

U.S. Auto Loan ABS Tracker: Full-Year And December 2018 Performance

Will the Froth in the U.S. Housing Market Bubble Over? We Think Not

10-Year Retrospective: Changes In U.S. Auto ABS In The Decade Since The Great Recession

What Blockchain Could Mean for Structured Finance

Marketplace Lending and the True Lender Conundrum

U.S. Commercial ABS Outlook For 2019: Generally Stable, But With Increased Volatility

Credit FAQ: When The Cycle Turns: Assessing How Weak Loan Terms Threaten Recoveries

Credit FAQ: The Key Ingredients For Whole Business Securitization Ratings

SF Credit Brief: Nissan Downgrade Expected To Have Minimal Impact On U.S. Auto ABS

Leveraged Finance: A 10-Year Lookback At Actual Recoveries And Recovery Ratings

CLO Spotlight: Sector Averages Of Assets Held In Reinvesting U.S. BSL CLOs: Fourth-Quarter 2018

Transaction-Specific 'B' Economic Stress Loss Projections For U.S. And Canadian CMBS Transactions As Of December 2018

CDO Spotlight: Performance Benchmarks For S&P Global Ratings-Rated CLO Transaction: Fourth-Quarter 2018

CLO Spotlight: The Most Widely Referenced Corporate Obligors In Rated U.S. CLOs: Fourth-Quarter 2018

As Boom In U.S. Lodging Industry Slows, CMBS Backed By Hotel Loans Face Changing Market Conditions

U.S. CMBS Conduit Update Q4 2018: Metrics Deteriorated A Bit, Stable Ratings Expected In 2019 With Some Caveats

Global Structured Finance Outlook 2019: Securitization Continues To Be Energized With Potential $1 Trillion in Volume Expected Again

Quarterly U.S. Credit Card Quality Index: Performance Remains Stable As Issuance Volume Declines

Is There Extension Tension In U.S. Subprime Auto Loan ABS?

Request For Comment: Global Methodology For Solar ABS Transactions

CLO Spotlight: European CLO Recovery Rates: Stability Continues Despite Deteriorating Credit Quality Of Leveraged Loans

CLO Spotlight: Although U.S. CLO Issuance Remained High, Rising Collateral Quality Pressures Resulted In A Cloudy Third-Quarter 2018

What's In Your CLO? A Second Deep Dive Into U.S. CLO Portfolios Highlights Deal Variance

U.S. FFELP Student Loan ABS: Methodology And Assumptions

Sector Averages Of Assets Held In Reinvesting U.S. BSL CLOs: Third-Quarter 2018

Credit FAQ: How We Rate Brazilian Covered Bonds

Extension Risk In Rated FFELP Student Loan ABS Transactions: FFELP Maturity Tracker September 2018

S&P Global Ratings' CLO Primer

Non-Qualified Mortgage Prepayments: Is It Life In The Fast Lane, Or Will They Start To Take It Easy?

Take Notes (available here)

On PACE For A Greener Future In Structured Finance

Conference Recap: CREFC 2019 And A Look Across The CMBS Market

The Lowdown On LatAm

Hot Takes From Opal’s 2018 CLO Summit

When You Use Your Whole Business To Securitize…

The "Unwoke" Millennial Housing Market

The Perfect Storm... For Defaults?

ABS East Recap

Recent Presales (available here)

U.S. ABS: SMB Private Education Loan Trust 2019-A

U.S. ABS: American Credit Acceptance Receivables Trust 2019-1

U.S. ABS: NextGear Floorplan Master Owner Trust (Series 2019-1)

U.S. ABS: AmeriCredit Automobile Receivables Trust 2019-1 (Cilento)

U.S. CMBS: CORE 2019-CORE Mortgage Trust

U.S. CLO: OCP CLO 2019-16 Ltd.

U.S. ABS: Verizon Owner Trust 2019-A

U.S. CLO: Anchorage Capital CLO 13 Ltd.

U.S. CLO: Ares LII CLO Ltd./Ares LII CLO LLC

APAC RMBS: Japan Housing Finance Agency Series 142

U.S. CMBS: Morgan Stanley Capital I Trust 2019-L2

U.S. ABS: Capital One Multi-Asset Execution Trust Class A (2019-1)

U.S. CLO: OHA Credit Funding 2 Ltd.

APAC RMBS: Pepper Residential Securities Trust No.23

Recent European Articles and Presales (available here)

Spanish Mortgage Loans IRPH Benchmark Index Under Scrutiny

German Covered Bond Market Insights 2019

Credit FAQ: How We Analyze Residential Mortgage Loans Backing Hungarian Covered Bonds

French Covered Bond Market Insights 2019

Changes Ahead: How Spain's New Mortgage Law Could Affect New And Outstanding RMBS Transactions

Spanish Covered Bond Market Insights

Countdown To Brexit: Uncertainty Created For Cross-Border Derivative Contracts Supporting Structured Finance Transactions

Global Covered Bond Characteristics And Rating Summary Q4 2018

New Issue: Income Contingent Student Loans 2 (2007-2009) PLC

Presale: STRONG 2018 B.V.

Presale: Salus (European Loan Conduit No. 33) DAC

New Issue: Citizen Irish Auto Receivables Trust 2018 DAC

|