2019 U.S. New Issuance in a Virtual Dead Heat With 2018 After a $48bn May (Erb/Manzi)

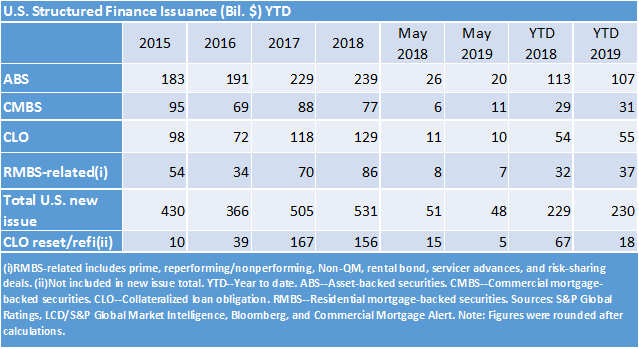

CMBS issuance was the standout in May, compared with declines in the other three major asset classes on a May 2019 over May 2018 basis. May’s structured finance (SF) new issuance volume came in at $48bn, down modestly from $51bn in the comparable year ago period. YTD 2019 new issuance is now just ahead of 2018, at $230bn (scroll down for table).

ABS new issuance volume came in at $20bn, off from $26bn last May. On a YTD basis, ABS issuance was $107bn, down about 6% y/y. Year-to-date auto ABS issuance (loan, lease, and rental car) is $52bn by our count, representing just under half of the total, and up about 13% y/y vs $46bn last year. Meanwhile, both cards and non-traditional/esoteric issuance are off from last year’s totals, at $11bn and $13bn, versus $19bn and $18bn a year ago. Commercial ABS (equipment, fleet, dealer floorplan), at $18bn YTD, is up about 7% y/y through the end of May. On the publication side, we recently releases our April auto loan ABS tracker and semi-annual Timeshare indices, both available here.

CLO new issuance volume was roughly $10bn in May, down 11% from May 2018. On a YTD basis however, CLO new issue volume was nearly unchanged from last year's figure, coming in at $55bn. Refis/reset/reissue volume continued to be substantially lower in May, down 66% y/y (May 2019 vs May 2018) and 73% YTD, coming in at $5bn and $18bn for May and YTD, respectively. Click here to view our recent CLO publications including our long awaited sequel to our popular article on CLO indenture provisions: Par Wars: Return of the Covenants? The article includes a "current status" update for each of the 10 CLO indenture items we identified in the original piece. Also, worth checking out — our CLO spotlight article, A Look Back At 15 Years Of U.S. BSL CLO Industry Exposures.

CMBS posted its largest monthly volume YTD, with $11bn in May bringing the 2019 figure to $31bn (we don’t count CRE CLOs in our NI total). That puts 2019 CMBS slightly ahead of the year ago figure of $29bn during the first five months. Our 2019 forecast remains at $80bn. Most of the $11bn in May came from the single borrower side, with over $7bn across 11 deals, bringing YTD SASB issuance to $16bn. Some $4bn in conduit issuance during May (four deals) brought the 2019 total thus far to $14bn (the remainder is small balance transactions). Click here to view our recent CMBS publications including Co-working May Come With Risks For Office Landlords And CMBS Investors.

PL-RMBS related issuance came in at $7bn in May. YTD RMBS related issuance is at $37bn, up 13% from this time last year. Non-qm issuance continues to have a strong year and is now approaching $8bn YTD, nearly double last year's figure. Click here to read our recent RMBS related publications including Key Factors For Assessing U.S. Non-Qualified Mortgage Bank Statement Loans.

Turning to the Numbers...

The 10yr Treasury was 2.13% for the week ending May 31, down from 2.33% last week. NYMEX crude oil was down $5.30 w/w to $53.33. U.S. regular gas prices averaged $2.83 this week, down 2 cents w/w and down 13 cents y/y. The S&P 500 was down 2.62% w/w to 2752.06. The 30-year fixed-rate mortgage decreased to 3.99%, down 7bps w/w (down 57bps y/y). The Euro was trading at $1.1168, down $0.0039 w/w.

Recent Presales (available here)

U.S. RMBS: Angel Oak Mortgage Trust 2019-3

U.S. ABS: Verizon Owner Trust 2019-B

U.S. ABS: Ally Auto Receivables Trust 2019-2

APAC RMBS: SMBC Residential Mortgage Trust Certificates No. 41/SMBC 41 RMBS ABL

U.S. CLO: Trimaran Cavu 2019-1 Ltd.

U.S. ABS: Welk Resorts 2019-A LLC

U.S. CLO: OHA Credit Funding 3 Ltd.

U.S. ABS: SMB Private Education Loan Trust 2019-B

U.S. RMBS: GCAT 2019-NQM1 Trust

U.S. CMBS: Morgan Stanley Capital I Trust 2019-H6

U.S. CLO: FS KKR MM CLO 1 LLC

U.S. CLO: HPS Loan Management 14-2019 Ltd./HPS Loan Management 14-2019 LLC

U.S. ABS: Illinois Finance Authority (Midwestern University Foundation) (Series 2019)

U.S. CLO: Owl Rock CLO I Ltd./Owl Rock CLO I LLC

U.S. ABS: Glendale Industrial Development Authority, Arizona (Midwestern University Foundation) (Series 2019)

Take Notes (available here) Co-Working On The Rise A New Office Space For CMBS And REITs

Covering New Ground: Covered Bonds Expand Into New Markets

Blockchain On The Brain

Across The Pond With European CMBS

Conference Recap: SFIG Vegas 2019

On PACE For A Greener Future In Structured Finance

Conference Recap: CREFC 2019 And A Look Across The CMBS Market

The Lowdown On LatAm

Hot Takes From Opal’s 2018 CLO Summit

When You Use Your Whole Business To Securitize…

The "Unwoke" Millennial Housing Market

The Perfect Storm... For Defaults?

ABS East Recap

Some $53bn in April Structured Finance New Issuance Pushes 2019 Ahead of 2018 Pace

$129bn in Q1 Issuance with $48bn in March

February Posts $48bn as Volatility Subsided

U.S. Structured Finance Issuance: January Was Slow to Start, But Picked Up Steam Heading Into February

Buyer Beware: The Curious Case of Income Supplemented BTL

Fewer Structural Protections in Today’s Speculative-Grade Subprime Auto Loan ABS

Recent In-Depth Articles (available here)

CLO Spotlight: European CLOs: Lack Of Loan Supply Is Causing Further Portfolio Overlap

Servicer Evaluation Spotlight Report™: Commercial Mortgage Servicers Deal with a Faulty but Functioning Flood Insurance Program

Credit FAQ: How We Rate Korean Covered Bonds

U.S. Auto Loan ABS Tracker March 2019

Spotlight On Italy's Securitization Market On The 20th Anniversary Of Law 130

CLO Spotlight: Once Upon A Time: A Look Back At 15 Years Of U.S. BSL CLO Industry Exposures

U.S. Timeshare Securitization Performance Index: New Issuance Grew In Second-Half 2018 As Defaults Remained Near 10-Year Average

Default, Transition, and Recovery: 2018 Annual U.S. Corporate Default And Rating Transition Study

New Issue: Dutch Property Finance 2019-1 B.V.

Swedish Covered Bond Market Insights 2019

Future Of Banking: Fintech Flags Turning Point For Australian Banking

Subprime Auto Loan ABS Tracker: Losses Have Stabilized, But Renewed Growth Bears Watching

U.S. Auto Loan ABS Tracker: February 2019

CLO Spotlight: Sector Averages Of Assets Held in Reinvesting U.S. BSL CLOs: First-Quarter 2019

Harmonization Accomplished: A New European Covered Bond Framework

Global Structured Finance Issuance Volumes For Q1 Steady As China Growth Offsets Declines In Europe And U.S.

Co-working May Come With Risks For Office Landlords And CMBS Investors

Key Factors For Assessing U.S. Non-Qualified Mortgage Bank Statement Loans

|