|

New Issuance at $39Bn in July; $315Bn YTD (Erb/Manzi/P. Desai)

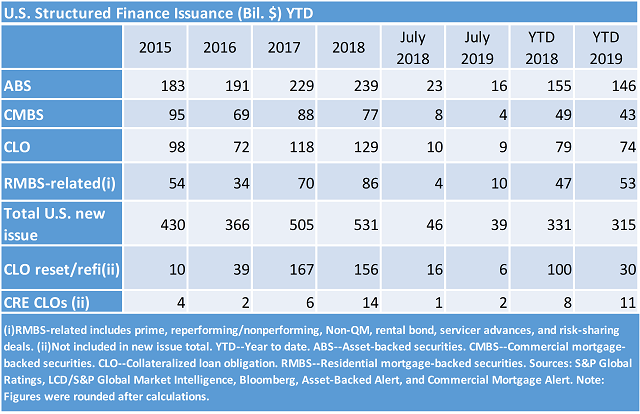

During July, U.S. Structured Finance (SF) new issuance volume reached $39bn, with $16bn in ABS, $4bn in CMBS, $9bn in CLOs, and $10bn in PL-RMBS. July issuance was down by about $7bn (down 15%) compared to last year's reading, with declines in ABS, CMBS, and CLOs. Led by growth in non-QM, RMBS new issue volume in July was over double last year's figure. Year-to-date (YTD), U.S. SF new issuance volume reached $315bn, down 5% from $331bn YTD 2018 (see table). July ABS new issuance came in at $16bn, down $7bn from last year's reading, led by a $3bn decline in credit card ABS issuance. Making up over half of July's issuance total, auto ABS issuance reached $9bn in July. The remaining issuance comprised $3bn in equipment/fleet lease, and $1bn apiece from cards, student loans, personal loans, and the non-traditional/esoteric subsector. YTD ABS issuance came in at $146bn, down 6% from 2018's figure. On the publication side, we recently released our May 2019 U.S. Auto Loan ABS Tracker and our commentary, U.S. Prime Auto Loan ABS Are Seeing More Back-Loaded Losses As Loan Terms Lengthen, which examines the impact that extended loan terms have on credit risk. CLO new issue volume was at $9bn in July and is at $74bn YTD, down 6% versus the comparable 2018 period. Relatively wide liability spread levels have held back CLO resets and refis, where issuance is down by over 70% y/y YTD. For more on CLOs, read our recent publications CLO Spotlight: The Most Widely Referenced Corporate Obligors In Rated U.S. BSL CLOs: Second-Quarter 2019 and U.S. Leveraged Finance Q2 2019 Update: 'B-' Issuer Credit Ratings on the Rise in Leveraged Loans and CLOs. CMBS issuance reached $4bn in July bringing the YTD figure to $43bn, down 13% y/y YTD. Nearly half of the total is from the single borrower side, although there was just one such pricing in July. We recently published U.S. CMBS Conduit Update Q2 2019: 'BBB-' Levels Remain Too Low where we examine loan metrics for U.S. conduit CMBS in Q2 2019. Private Label RMBS-related issuance reached $10bn in July, over double last year’s reading of $4bn. YTD, issuance is up 11% on a year-over-year basis for 2019 and is now at $53bn. Non-QM continues to have a strong year and is currently at about $13bn YTD, over double 2018's figure. For more RMBS coverage, read Can Australian RMBS Ratings Withstand A Slowing Economy And Lower Property Prices? where we examine the relationship between Australia's changing macroeconomic environment and RMBS ratings.

Turning to the Numbers

The 10yr Treasury was 1.84% for the week ending August 2, down from 2.07% last week. NYMEX crude oil was down $0.99 w/w to $55.21. U.S. regular gas prices averaged $2.72 this week, down 3 cents w/w and down 15 cents y/y. The S&P 500 was down 3.1% w/w to 2932.05. The 30-year fixed-rate mortgage was unchanged w/w at 3.75% (down 85bps y/y). The Euro was trading at $1.1132, down $0.0089 w/w.

H1 2019 U.S. New Issuance Volume at $275bn; Off 4% Y/Y

2019 U.S. New Issuance in a Virtual Dead Heat With 2018 After a $48bn May

Some $53bn in April Structured Finance New Issuance Pushes 2019 Ahead of 2018 Pace

$129bn in Q1 Issuance with $48bn in March

February Posts $48bn as Volatility Subsided

U.S. Structured Finance Issuance: January Was Slow to Start, But Picked Up Steam Heading Into February

Buyer Beware: The Curious Case of Income Supplemented BTL

Fewer Structural Protections in Today’s Speculative-Grade Subprime Auto Loan ABS

Recent In-Depth Articles (available here)

Second-Quarter 2019 Non-Model CDO Monitor Benchmarks Reveal Relative Credit Quality And Diversity Of CLO Portfolios

U.S. Credit Card Quality Index: Monthly Performance - June 2019

U.S. Leveraged Finance Q2 2019 Update: 'B-' Issuer Credit Ratings On The Rise In Leveraged Loans And CLOs

Japanese Securitizations' 2019 First Half Rated New Issuance Worth About ¥1 Trillion; One Upgrade And One Downgrade

Can Australian RMBS Ratings Withstand A Slowing Economy And Lower Property Prices?

U.S. Prime Auto Loan ABS Are Seeing More Back-Loaded Losses As Loan Terms Lengthen

Servicer Evaluation Spotlight Report™: The Digital Age Of Residential Mortgage Customer Service

U.S. Auto Loan ABS Tracker: May 2019

When The Credit Cycle Turns: Recovery Prospects In The U.S. Technology Sector

The U.S. Auto Industry's Historic Sales Run Will Taper Off Over The Next 12-24 Months; Negative Rating Bias Could Intensify Somewhat

Global Securitization Issuance Remains On Track For $1 Trillion-Plus After A Robust First Half

Danish Covered Bond Market Insights 2019

CLO Spotlight: Something Old, Something New: Meet The CLO MASCOT

U.S. CMBS Conduit Update Q2 2019: 'BBB-' Levels Remain Too Low

The Most Widely Referenced Corporate Obligors In Rated U.S. BSL CLOs: Second-Quarter 2019

U.S. Credit Card Quality Index: Monthly Performance - May 2019

Global Covered Bond Insights Q2 2019

Global Covered Bond Characteristics And Rating Summary Q2 2019

S&P Global Ratings' Covered Bonds Primer

Easy Credit Fuels Growth In U.S. Middle Market CLO Loans

S&P Global Ratings' Covered Bonds Primer

U.S. Auto Loan ABS Tracker: April 2019

Cycle Turn Will Test European CLO 2.0 Defaults

Credit FAQ: Questions Over Electric Vehicle Residual Values In European Auto ABS

CLO Spotlight: European CLOs: Lack Of Loan Supply Is Causing Further Portfolio Overlap

Servicer Evaluation Spotlight Report™: Commercial Mortgage Servicers Deal with a Faulty but Functioning Flood Insurance Program

Credit FAQ: How We Rate Korean Covered Bonds

|