|

U.S. Structured Finance New Issuance Volume at $50bn in Sep., $129Bn in Q3 2019 and $409Bn YTD (Erb/Manzi)

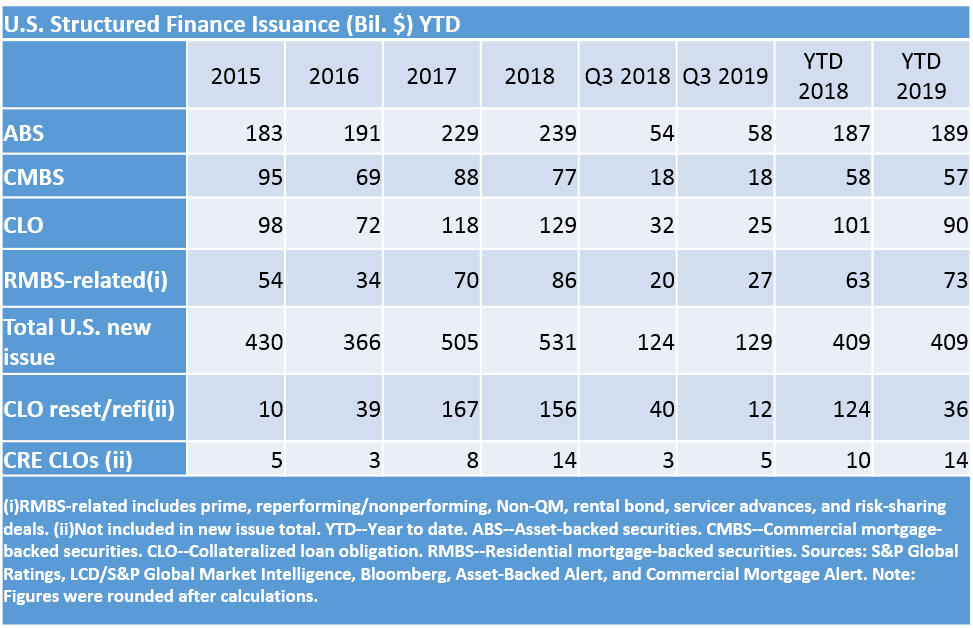

U.S. Structured Finance (SF) new issuance volume reached $50bn in Sep, comprising $25bn ABS, $9bn CMBS, and $8bn apiece for CLOs and RMBS. On a y/y basis, the $129bn in issuance during Q3 was up 4%, and the $409bn YTD was equal to 2018's pace, although the composition was somewhat different. Following last year's record new issue CLO volume, that sector has seen a modest decrease y/y, while RMBS (notably, Non-QM) has made up the difference. Following a busy September ($25bn, second only to April), ABS issuance reached $58bn in Q3 2019, up by about $4bn from Q3 2018, with Auto ABS up by $2bn, CCABS down by $1bn, esoteric ABS up by $2.5bn, and student loan ABS down by $2bn. YTD ABS issuance was up 1% at the end of September, at $189bn. On the publication side we recently released our July 2019 U.S. Auto Loan ABS Tracker, an article exploring data center securitizations: Field Of Data Streams: If You Build It, They Will Come, and an article and podcast on the topic of student loan forgiveness. CLO new issuance came in at $25bn in Q3 2019, down by about $8bn from Q3 2018. YTD CLO new issuance stands at $90bn, down from $101bn last year (which set an annual record) at the end of September. CLO reset/refi volume remains down, with Q3 volume reaching $12bn, down by about 70% from $40bn in Q3 2018 (YTD issuance, at $36bn, is also down by about 70% y/y). For more on CLOs, read our recent publications Twenty-Five Years Strong: Update On CLO 1.0 Defaults and Q2 Credit Estimates Within Middle Market CLOs. We've also recently released a podcast on CLO documentation, available here. CMBS issuance reached $18bn in Q3, flat year-over-year from Q3 2018, with about half of the volume coming in a busy September. We expect an active market in Q4, and reiterate the $80bn forecast that we published in January 2019. CMBS new issuance YTD is now at $57bn, down just $1bn from last year's reading. The slight decline is attributable to lower SASB and SB (small balance) issuance, which combined, were down by about $4bn YTD at the end of September. This was offset, however, by a $3bn increase in conduit issuance. (Note that we do not include CRE CLOs in our CMBS new issue totals.) On the CMBS publication front, we recently published a credit FAQ examining the recent increase in AAA (sf) rated A-S and A-M classes.

Private label RMBS-related issuance reached $27bn in Q3, up 38% from $20bn in Q3 2018, with some $4bn of the uptick attributable to an increase in non-QM issuance. YTD RMBS issuance was up by 15%, reaching $73bn at the end of September. For more RMBS coverage, read our recent publication Non-QM's Meteoric Rise Is Leading The Private-Label RMBS Comeback, and listen to our recent podcast on Investor Property DSCR Loans.

As you may have noticed we have made some exciting updates to our website, www.spglobal.com/ratings. The content within our email is free to view but requires registration to be accessed. Registration takes less than a minute.

Recent Presales (available here)

LatAm Repack: Rutas 2 And 7 Finance Ltd. Series 2019-1

U.S. CLO: Madison Park Funding XXXIII Ltd.

U.S. RMBS: NRZ Advance Receivables Trust 2015-ON1 Series 2019-T4

U.S. CLO: OHA Credit Funding 4 Ltd.

U.S. ABS: MVW 2019-2 LLC

U.S. ABS: Volkswagen Auto Lease Trust 2019-A

U.S. ABS: World Omni Select Auto Trust 2019-A

APAC ABS: Silver Arrow Australia 2019-1

Recent EMEA Presales

MacKay Shields Euro CLO-1 DAC

Autonoria 2019 FCT

Dowson 2019-1 PLC

Genesis Mortgage Funding 2019-1 PLC

GREEN STORM 2019 B.V.

ASR Media And Sponsorship S.p.A.

York Potash Intermediate Holdings PLC

Hawksmoor Mortgage Funding 2019-1 PLC

MV24 Capital B.V.

Westfield Stratford City Finance No.2 PLC

Take Notes (available here) U.S. Student Loans: Should We Forgive And Forget?

What's Up (CLO) Docs?

What Are Investor Property DSCR Loans

Conference Recap: European Structured Finance Conference 2019

The Evolution Of Marketplace Lending

RMBS Down Under

Conference Recap: Global ABS In Barcelona

What’s Heating Up in the Solar ABS Space

Conference Recap: IMN CLO Conference 2019

Co-Working On The Rise A New Office Space For CMBS And REITs

Covering New Ground: Covered Bonds Expand Into New Markets

Blockchain On The Brain

Across The Pond With European CMBS

August Brings $39bn in Issuance; YTD Total Down 5% Y/Y

New Issuance at $39Bn in July; $315Bn YTD, Down 5% Y/Y

H1 2019 U.S. New Issuance Volume at $275bn; Off 4% Y/Y

2019 U.S. New Issuance in a Virtual Dead Heat With 2018 After a $48bn May

Some $53bn in April Structured Finance New Issuance Pushes 2019 Ahead of 2018 Pace

$129bn in Q1 Issuance with $48bn in March

February Posts $48bn as Volatility Subsided

U.S. Structured Finance Issuance: January Was Slow to Start, But Picked Up Steam Heading Into February

Buyer Beware: The Curious Case of Income Supplemented BTL

Fewer Structural Protections in Today’s Speculative-Grade Subprime Auto Loan ABS

Recent In-Depth Articles (available here)

Coming Out Of A Pit Stop, Could Mexican Auto Loan Securitization Retake Its Lost Position?

U.S. Auto Loan ABS Tracker: July 2019

Field Of Data Streams – If You Build It, They Will Come

Non-QM's Meteoric Rise Is Leading The Private-Label RMBS Comeback

The Continued Attack Of The EBITDA Add-Back

After Volatility In 2016, Timeshare Performance Seems To Find A 'New Normal' In First-Half 2019

ESG Credit Factors in Structured Finance

Global Auto Sales Will Stay in the Slow Lane for at Least the Next Two Years

Use of GICs Industry Categories in SPGR-Rated CLOs Updated

Speed Bump Ahead: As Auto Loans Accelerate Toward 84 Months, Caution Is Warranted

Q2 Credit Estimates Within Middle Market CLOs

The Role Of Environmental, Social, And Governance Credit Factors In Our Ratings Analysis

Highlights From S&P Global Ratings’ 2019 European Structured Finance Conference

Global Covered Bond Insights Q3 2019

Global Covered Bond Characteristics And Rating Summary Q3 2019

Credit FAQ: Are Covered Bonds Becoming More Sustainable?

CLO Spotlight: Closing The Low European CLO 1.0 Default Chapter, Onto The Next

The Problem with Student Loan Forgiveness for All

The Credit Effects Of The Temporary QM Patch Expiration On The U.S. Mortgage Market

U.K. Mortgage: Will Innovation Give The U.K. Mortgage Market A Boost?

When The Cycle Turns: How Would Global Structured Finance Fare In A Downturn?

More Than One-Third Of U.K. Legacy Borrowers Are "Mortgage Prisoners"

Game Of Loans: The Nitty-Gritty Of Granular European CMBS Transactions

|